An Investor's Guide to Property Investment

DOWNLOAD THE GUIDE

Residential property investments

Property investment styles

Stella, a buy-to-let landlord

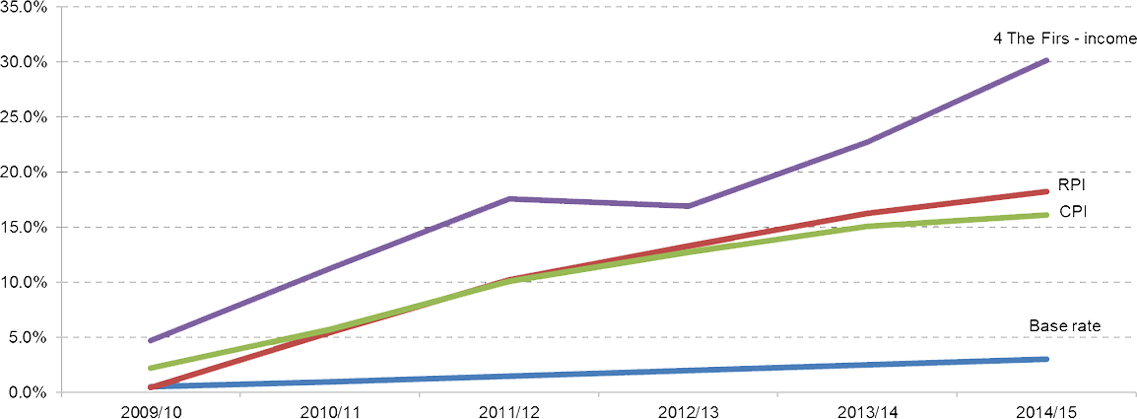

Stella sold 4 The Firs in April 2015. She achieved a total net yield of 30.2% over six years; an average net yield of 5.0% per year. Figure 3 shows that this yield comfortably exceeds the Bank of England base rate, to which deposit account interest rates are pinned. It also exceeds both the Consumer Price Index (CPI) and the Retail Price Index (RPI). Based solely on net income, the investment has increased in value in real terms over the six-year period.

When Stella sold 4 The Firs in April 2015, she achieved a sale price of £142,000; £7,000 more than she paid for it in April 2009. As with the income she received when the property was let, selling the property incurs costs. Stella pays an estate agent 1% of the sale price, a solicitor £750 to cover conveyance costs, and because 4 The Firs is not her main residence, the increase in value is also liable for capital gains tax.

An Investor's Guide to Property Investment

DOWNLOAD THE GUIDE

Caroline and Martin, property crowdfunding investors

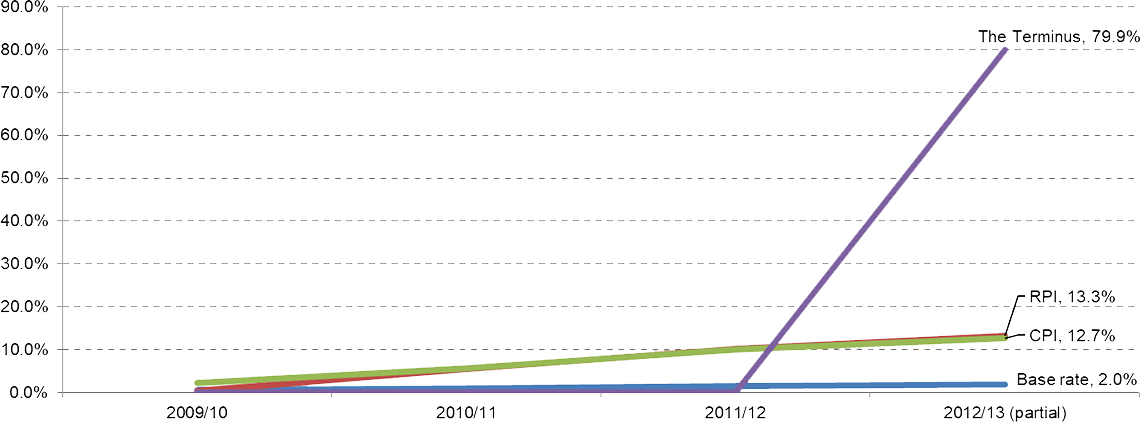

The Terminus encountered some delays during the construction phase. Nonetheless, the final apartment was sold in May 2012, and the development was completed in July 2012. The total revenue generated through sales was £21.2 million and, once construction and management/administration costs had been accounted for, the special purpose vehicle was left with £14.99 million to distribute to investors. This was allocated and repaid in September 2012. Caroline received £27,750 through this process, representing a 1.85x return on her initial investment, across 42 months. The Terminus fell slightly short of its anticipated financial return (1.9x) and completed six months behind schedule.

When Caroline received her investment return, its increase in value (£12,750) was liable for capital gains tax. The personal capital gains tax-free allowance of £10,600 in the 2012/13 left Caroline with a taxable gain of £2,150. This taxable gain incurred capital gains tax at 18%, as Caroline was a standard rate taxpayer, resulting in a capital gains tax bill of £387. Allowing for Caroline’s investment initiation fee of £375 and her capital gains tax bill of £387, her net gain was £11,988. This represents a net 1.80x return on her initial investment. This comfortably outperforms the inflation indices (RPI and CPI) and the Bank of England’s base rate (Figure 6). Figure 6 also demonstrates that the investment offers no return during the first two financial years, with the full return received in the third year. Caroline’s investment in The Terminus generates an IRR of 18.3%. Despite achieving a return that exceeded that of Meadow View, the IRR offered by The Terminus is inferior; this is because the development took longer to complete. From a capital gains tax perspective, Martin and Caroline’s decision to make one investment each was immaterial. This is because the two investments matured in different financial years: Martin’s in Meadow View in 2011/12 and Caroline’s in The Terminus in 2012/13. Had one of them made both investments, they could have used their personal capital gains tax-free allowances in each respective year. Had the two investments matured in the same financial year, holding one investment each would have been materially beneficial to their outturn